Ohio property owners often experience confusion when reviewing their annual property tax bills. When the county auditor releases your updated property valuation, the final amount you owe is never calculated directly from that top-line market price. Instead, Ohio utilizes a strict statutory adjustment mechanism known as the 35% assessment ratio. This formula bridges the gap between your property’s real-world market value and its legally taxable base. For real estate investors, local homeowners, and professionals, understanding the history, calculation, and mechanics behind this specific assessment percentage is critical to managing annual real estate liabilities. This guide provides an expert, comprehensive dive into the structure of Ohio’s property tax baseline and explains how local administrative frameworks execute this formula across different taxing districts.

The Historical Origin of the 35% Assessment Ratio in Ohio

The assignment of property tax burdens to a fractional portion of market value is not a random administrative preference. It is an intentional framework established through a combination of constitutional mandates, statutory laws, and historic judicial oversight.

Constitutional Roots and Judicial Intervention

The Ohio Constitution has required property to be taxed by uniform rules according to value since 1851. However, historically, different counties deployed varying assessment ratios, which caused significant disparities in school funding and local tax burdens across the state. To rectify this lack of uniformity, the Ohio Department of Taxation and the state legislature formalized the assessment ratio system under Ohio Revised Code (ORC) Sections 5713.03 and 5715.01.

Standardizing the Ratio

Through a series of legislative updates, the state standardized real property assessment at exactly 35% of true market value. By locking in a uniform percentage statewide, Ohio ensured that a home appraised at a specific price point in an urban center would share a legally identical taxable foundation with an identically valued home in a rural township. This uniform assessment baseline provides structural equity across all 88 independent Ohio counties.

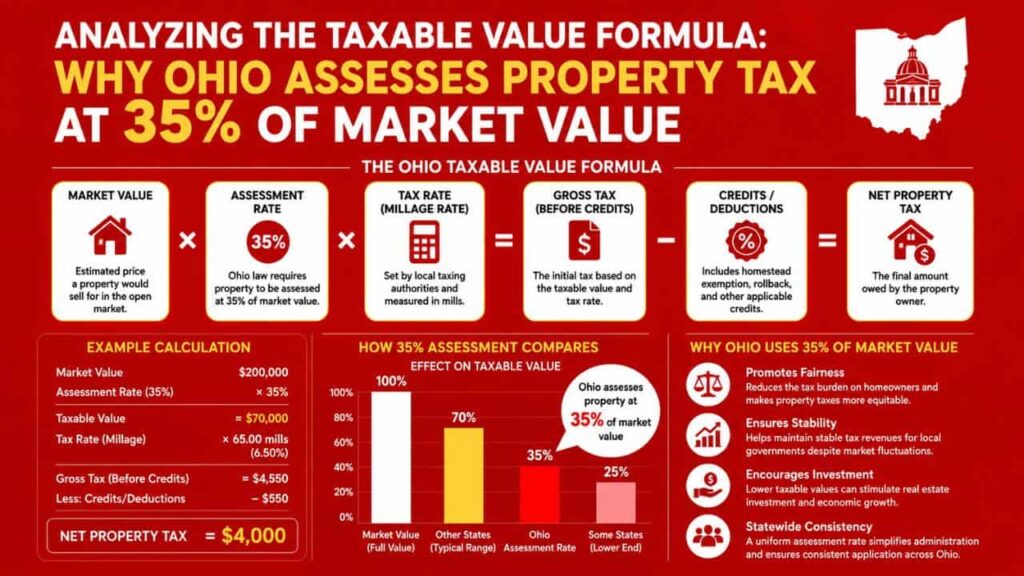

Breaking Down the Mathematical Taxable Value Formula

To successfully audit your property tax statement, you must understand how your county auditor converts your raw market value into a baseline taxable amount. The formula relies entirely on the interplay between three factors: Appraised Market Value, the Assessment Ratio, and your local Millage Rate.

Step 1: Converting Appraised Value to Assessed Value

The county auditor determines your property’s fair market value based on recent local arm’s-length sales, physical attributes, and regional location metrics. Once that baseline is set, the 35% factor is applied:

Assessed Taxable Value = Appraised Market Value x 0.35

Step 2: Applying the Millage Rate

Your tax bill is charged in mills. One mill is equal to one-thousandth of a dollar, which equates to $1 of tax liability for every $1,000 of your assessed taxable value (not your total market value).

Comparing Data Infrastructure and Regional Auditor Roles

While the 35% assessment ratio is mandated uniformly by state law, the task of executing appraisals, tracking property records, and presenting data falls on local county auditors. These officials serve as the frontline fiscal watchdogs for your community’s real estate data.

For example, the Trumbull County Auditor manages the digital mapping layers and tax data arrays for over 100,000 regional parcels, ensuring that local school district levies align correctly with individual parcel boundaries.

When analyzing how this data infrastructure operates across Ohio, comparing systems with other prominent regional frameworks reveals how standardized data structures function.

| Property Assessment Data Component | Statutory State Framework | Local Portal Infrastructure (e.g., Trumbull County) | Comparative Portal Infrastructure (e.g., Stark County) |

| Assessment Ratio Application | Mandated at exactly 35% by Ohio Revised Code. | Built into automated database calculation scripts for all parcels. | Applied uniformly across all residential and commercial profiles. |

| Appraisal & Valuation Cycles | Sexennial full reappraisal required every 6 years; triennial update at midpoint. | Coordinates field inspections and processes local conveyance data. | Manages data validation to provide a structured guide for auditor services. |

| Millage & Levy Integration | Administered alongside House Bill 920 reduction factors. | Integrates township and municipal service boundaries into GIS mapping. | Tracks voter-approved fixed-rate and fixed-sum levy benchmarks. |

Step-by-Step Guide: How to Verify Your Taxable Assessment Base

If you want to ensure your property tax calculations are perfectly aligned with official state parameters, follow this professional step-by-step audit sequence.

Step 1. Extract Your Appraised Fair Market Value: Value Verification.

Log onto your county auditor’s property search platform. Enter your parcel ID or physical address to view the current market value established during the latest triennial update or sexennial reappraisal cycle.

Step 2. Calculate Your Assessed Taxable Value Baseline: Formula Execution.

Multiply the recorded market value by 0.35. For instance, if your property is appraised at $200,000, your final calculated result must equal exactly $70,000.

Step 3. Match the Calculated Value to Your Physical Tax Bill: Statement Comparison.

Open your latest statement from the County Treasurer. Compare your manual calculation against the amount printed under the “Taxable Value” or “Assessed Value” section of the document.

Step 4. File an Administrative Complaint If Values Misalign: Discrepancy Correction.

If the listed taxable baseline exceeds 35% of your recorded market appraisal, contact the auditor’s appraisal department immediately or file an official dispute with the local Board of Revision using DTE Form 1 before March 31.

Go to the Legal Protections and Operational Tax Relief Programs

The 35% assessment ratio works in tandem with several legal protections passed by the Ohio General Assembly to ensure that your annual real estate bill remains predictable, fair, and stable.

- The House Bill 920 Reduction Factor:

This statutory measure scales down effective millage rates when aggregate property values rise inside a taxing district, preventing local schools and municipal governments from receiving automatic windfall revenues from inflation. - The 2.5% Owner-Occupancy Reduction:

Homeowners who own and occupy their property as their principal place of residence are eligible for a 2.5% tax reduction on eligible local levies, which applies directly against their assessed value calculations. - The Homestead Exemption Program:

Senior citizens aged 65 or older and permanently disabled individuals who meet income guidelines can shield the first $26,200 (or up to $52,400 for qualifying disabled veterans) of market value from the 35% assessment calculation entirely.

Conclusion

Navigating Ohio property tax formulas requires a clear grasp of the 35% assessment ratio mandated under the Ohio Revised Code. By converting fair market valuations into an assessed taxable value, this framework ensures statewide property uniformity. Utilizing official digital platforms managed by the Trumbull County Auditor or Stark County Auditor allows property owners to audit their statements, track local school levies, and seamlessly leverage state-level tax reduction programs.

FAQs

Why does Ohio use a 35% assessment ratio for real estate taxes?

Ohio uses the 35% ratio to standardize property tax bases across all 88 counties, ensuring uniform compliance with constitutional mandates and predictable municipal and school district funding.

What is the formula to find my property’s taxable value?

Take the total fair market value determined by your county auditor and multiply it by 0.35. Your final local millage rate is applied strictly to this resulting amount.

Does the Stark County Auditor use the same 35% formula as Trumbull County?

Yes. Every independent county auditor across the state of Ohio is legally required by the Department of Taxation to calculate property taxes using the exact same 35% assessment ratio.

How often are property market values updated by the county auditor?

County auditors conduct a full physical reappraisal of all real property every six years, with a statistical triennial update calculated at the three-year midpoint of the cycle.

Can I appeal my property’s assessed value if it is too high?

Yes. Property owners can file a formal valuation complaint with their local Board of Revision using DTE Form 1 between January 1 and March 31 of each calendar year.