Ohio real estate markets are preparing for major administrative updates as upcoming mass reappraisals loom across several regions. For property owners, a state-mandated property re-valuation triggers an immediate shift in annual tax liabilities. These valuation adjustments determine whether your local tax bills spike or stabilize. Because Ohio property tax calculations rely on accurate, updated fair market values, navigating the mass appraisal timeline can mean the difference between financial stability and unexpected budgetary strain. This comprehensive guide covers how county authorities calculate your property values, how tax rates change, and how to protect your assets when new valuation notices hit your mailbox.

What is an Ohio Mass Reappraisal?

Under the Ohio Revised Code (ORC), every county must establish uniform and equalized property values across all parcels. To achieve this, Ohio utilizes an alternating six-year assessment cycle managed directly by county authorities.

The Sexennial Reappraisal vs. The Triennial Update

A full Sexennial Reappraisal occurs every six years. During this cycle, county auditors deploy specialized Computer-Assisted Mass Appraisal (CAMA) software and physical data collectors to evaluate every residential, commercial, and agricultural property. The goal is to accurately calculate the current fair market value based on structural conditions, lot sizes, and neighborhood improvements.

Conversely, a Triennial Update occurs at the three-year midpoint of this cycle. Triennial updates do not require physical, exterior property inspections. Instead, auditors execute statistical adjustments using recent local real estate sales data from the preceding three years to align older assessments with shifting market trends.

Trumbull County vs. Stark County: Operational Management

Understanding how these massive appraisal projects are managed locally highlights the importance of office infrastructure. For instance, Trumbull County Auditor Martha Yoder recently initiated a comprehensive request for proposals (RFP) to upgrade the county’s core CAMA real estate and property taxation system. This upgrade ensures advanced modeling for the region’s upcoming $2.1 million valuation project.

Looking at neighboring regions provides an excellent blueprint for how these independent offices maintain public transparency during complex state-mandated appraisal cycles.

| County Administrative Entity | Primary Valuation Accountability | Real Estate Software & Appraisal Scope | Local Oversight & System Status |

| Trumbull County Auditor | Manages a $2.1M mass reappraisal project and local valuation updates. | Deploying updated CAMA system software to model shifting real estate values. | Governed by the Ohio Department of Taxation to maintain legal compliance. |

| Stark County Auditor | Administers countywide assessments and provides a comprehensive services guide. | Coordinates rolling statistical adjustments and automated property parcel lookups. | Operates as an independent fiscal watchdog ensuring uniform local property values. |

| Board of Revision (BOR) | Hears formal complaints regarding inaccurate property tax valuations. | Reviews independent property appraisals, recent sales deeds, and photos. | Serves as the official legal avenue for property owners to appeal tax values. |

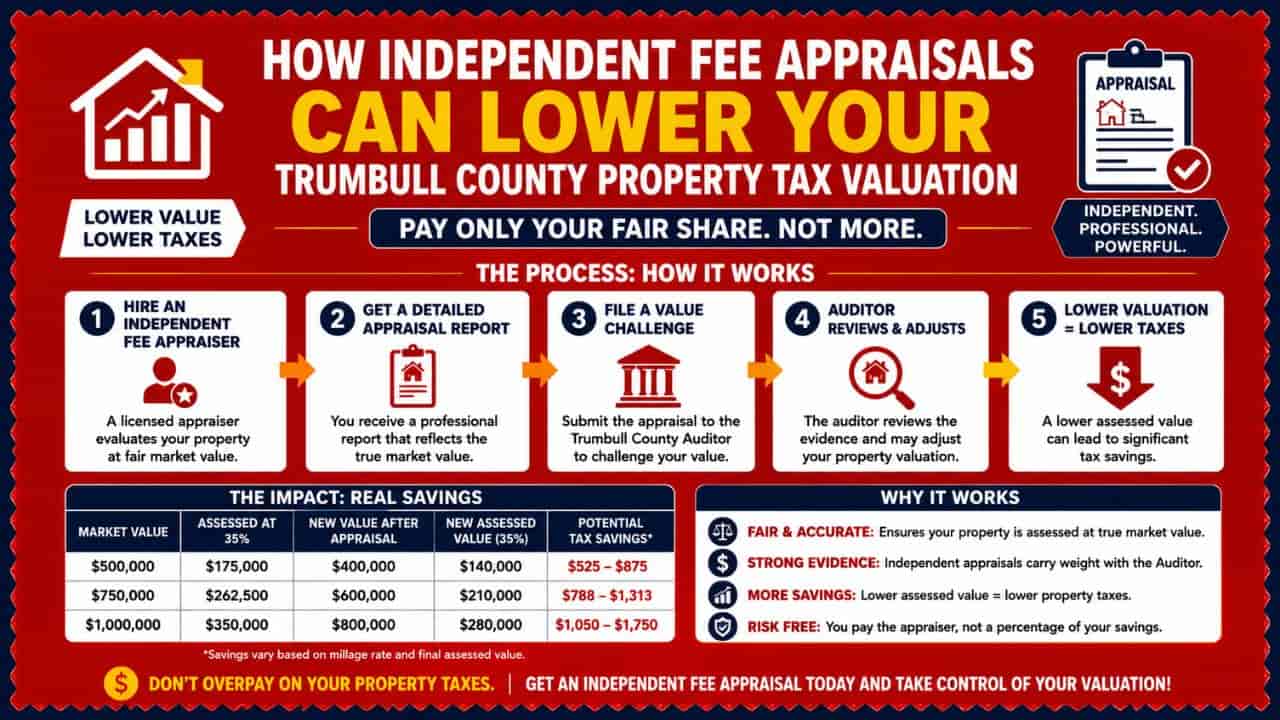

Step by Step Guide: How the Mass Reappraisal Process Works

When an Ohio county undergoes a complete reassraisal, the workflow follows a highly regulated administrative sequence. Understanding these steps allows you to prepare for changes well before your new tax bill arrives.

Phase 1 .Market Data Collection and CAMA System Modeling: Data Gathering.

Appraisal contractors and county technicians gather valid, arm’s-length sales data across every neighborhood. They track home improvements, building permits, and structural demolitions to update the primary real estate database.

Phase 2 .Field Inspections and Initial Property Valuations: Valuation Analysis.

For sexennial reappraisals, appraisers perform external checks to verify the property’s physical condition. The information is processed through the county’s specialized taxation software to establish a preliminary fair market value.

Phase 3.Ohio Department of Taxation Review and Approval: State Verification.

The county auditor submits the preliminary aggregate values to the state tax commissioner. The state reviews the data against macroeconomic trends to ensure the county’s adjustments comply with uniform equalization laws.

Phase 4. Mailing Value Notices and Informal Review Openings: Public Notification.

Once approved, the auditor’s office sends official valuation notices to all property owners. Residents can then participate in informal review sessions to correct obvious data errors before values are locked.

How Property Value Adjustments Impact Your Tax Bill

A common misconception among local property owners is that a 30% increase in property value automatically triggers a 30% increase in real estate taxes. This is rarely the case due to Ohio’s unique tax protection laws.

The Role of House Bill 920 (HB 920)

Passed into law to protect homeowners from runaway inflation, House Bill 920 automatically reduces effective tax millage rates as property values rise across a taxing district. This mechanism ensures that voter-approved, fixed-dollar levies do not collect excess revenue simply because the local real estate market boomed.

Calculating Your Assessed Value

In Ohio, you do not pay taxes on 100% of your property’s market value. Your assessed value or taxable value is strictly limited to 35% of the total appraised fair market value.

Taxable Value = Appraised Fair Market Value x 0.35

If the upcoming mass reappraisal sets your home’s market value at $200,000, your local taxes will be calculated using a taxable base of $70,000, multiplied by the total effective millage rate of your specific local precinct.

Step by Step Solution: Resolving an Inaccurate Valuation

If you receive your new valuation notice and believe the auditor’s office overvalued your property, you have a direct, legal method to contest the assessment and lower your potential tax burden.

- Step 1: Check Local Sales Data:

Use your county auditor’s online portal or GIS parcel viewer to examine recent sales of similar homes in your immediate neighborhood. If nearby homes sold for less than your new appraised value, you have a strong case. - Step 2: File a Counter-Complaint:

Gather supporting documentation, such as a recent independent fee appraisal, structural engineering reports detailing defects, or clear interior and exterior photographs showing property damage. - Step 3: Submit a Formal Appeal to the Board of Revision (BOR):

File an official Complaint Against the Valuation of Real Property (Form DTE 1) with your local county BOR. These applications must be submitted between January 1 and March 31 of the year following the valuation update. - Step 4: Present Evidence at the Hearing:

Attend your scheduled BOR hearing to present your facts to the board members. If your documentation proves the market value is lower than the auditor’s calculation, the board will issue a formal credit adjustment to lower your real estate taxes.

Conclusion

Managing the upcoming Ohio mass reappraisal effectively ensures long-term fiscal accuracy for all local property owners. Whether tracking updates from the Trumbull County Auditor or reviewing general Stark County Auditor procedures, state-mandated property valuations directly dictate your annual real estate taxes. By actively monitoring valuation cycles, understanding taxable value formulas, and engaging with the local Board of Revision, you can secure fair assessments and protect your real estate assets.

FAQs

What is an Ohio mass reappraisal?

It is a state-mandated sexennial review where the county auditor establishes updated fair market values for every property parcel to ensure uniform local real estate taxation.

How is my property taxable value calculated in Ohio?

Your taxable value is strictly limited to 35% of the total appraised fair market value determined by your local county auditor during the mass reappraisal cycle.

Will a higher property appraisal automatically spike my tax bill?

No. Under Ohio’s House Bill 920, effective millage rates decrease as property values rise across a taxing district, protecting property owners from runaway tax inflation.

How can I challenge an inaccurate property valuation notice?

You must file DTE Form 1 with your county Board of Revision between January 1 and March 31 to formally dispute an overvalued property assessment.

What role does CAMA software play in valuation updates?

County auditors deploy advanced Computer-Assisted Mass Appraisal software to analyze recent neighborhood sales trends and generate precise, equitable market valuations countywide.