When Trumbull County completes its triennial property tax updates, many local real estate owners discover an unsettling truth: automated mass appraisal models frequently overestimate true market value. If a rising tide of localized property sales has artificially inflated your tax bill, you do not have to accept the county’s valuation as the final word. Securing an independent fee appraisal provides the objective, legally defensible evidence needed to challenge an overassessed property valuation before local administrative boards.

The Conflict in Property Valuation: Mass Appraisal vs. Fee Appraisal

Understanding why property tax assessments get out of alignment requires looking closely at how local government entities calculate real estate values. Administrative offices must balance scalability with localized precision.

The Standard Mass Appraisal System

Every three to six years, Ohio county auditors are legally required to refresh local tax duplicates. To achieve this cost-effectively across tens of thousands of parcels, the Trumbull County Auditor relies on a methodology known as computer-assisted mass appraisal (CAMA). Instead of walking through your home, data algorithms sort properties by broad neighborhoods, square footage ranges, and basic age brackets.

Because CAMA systems look strictly at macro-level trends, they cannot identify isolated internal defects, layout obsolescence, or micro-market real estate shifts that decrease the marketable value of an individual property.

Why an Independent Fee Appraisal Overrides Mass Models

An independent fee appraisal provides a comprehensive, granular analysis of a specific real estate asset. Conducted by an Ohio-credentialed, licensed professional, a private fee appraisal provides an unbiased valuation based on direct physical inspection and exact structural matching.

When you file an appeal, administrative boards evaluate the specific evidence provided. A certified appraisal report adhering strictly to the Uniform Standards of Professional Appraisal Practice (USPAP) naturally carries significant legal weight, successfully counterbalancing the state’s automated calculations.

How Ohio County Auditors Approach Valuation Appeals

The statutory mechanics of real estate valuation remain consistent across the state of Ohio, yet local adjustments depend entirely on individual county timelines.

The Local Board of Revision Framework

Under Ohio Revised Code (ORC) Section 5715.19, property owners can formally contest their property valuations by filing a complaint with the county Board of Revision (BOR). The board functions as a quasi-judicial hearing body consisting of three specific local officials or their representatives:

- The County Auditor

- The County Treasurer

- The President of the Board of County Commissioners

The BOR reviews real estate proof to decide if the auditor’s tax duplicate value reflects true market conditions as of the tax lien date (January 1st of the tax year in question).

The Broader Ohio Context: Trumbull vs. Stark County Operations

While administrative frameworks remain unified by state law, county tax update schedules differ. For instance, the Stark County Auditor manages real estate adjustments on a completely separate triennial rotation than Trumbull County.

Property owners should note that during high-volume update cycles, both counties see a substantial influx of BOR filings. No matter the county, local administrative panels follow identical evidentiary rules: they will routinely dismiss casual online pricing estimates, instead favoring formal, localized valuation documents compiled by an independent expert appraiser.

Key Evaluation Metrics in an Independent Appraisal Report

To secure a property tax deduction, an appraisal report must analyze specific market segments. Certified real estate appraisers use multiple valuation pillars to determine true value.

| Valuation Metric Component | Administrative Data Collection Source | Localized Real Estate Impact |

| Sales Comparison Approach | Verified arm’s-length transactions from local MLS records. | Adjusts for exact proximity, date of sale, and square footage anomalies. |

| Physical Condition Adjustments | In-person structural, mechanical, and roof safety inspections. | Quantifies unaddressed deferred maintenance costs to reduce taxable value. |

| Functional Obsolescence | Architectural design and neighborhood layout analysis. | Accounts for odd floor plans or adjacent commercial noise nuisances. |

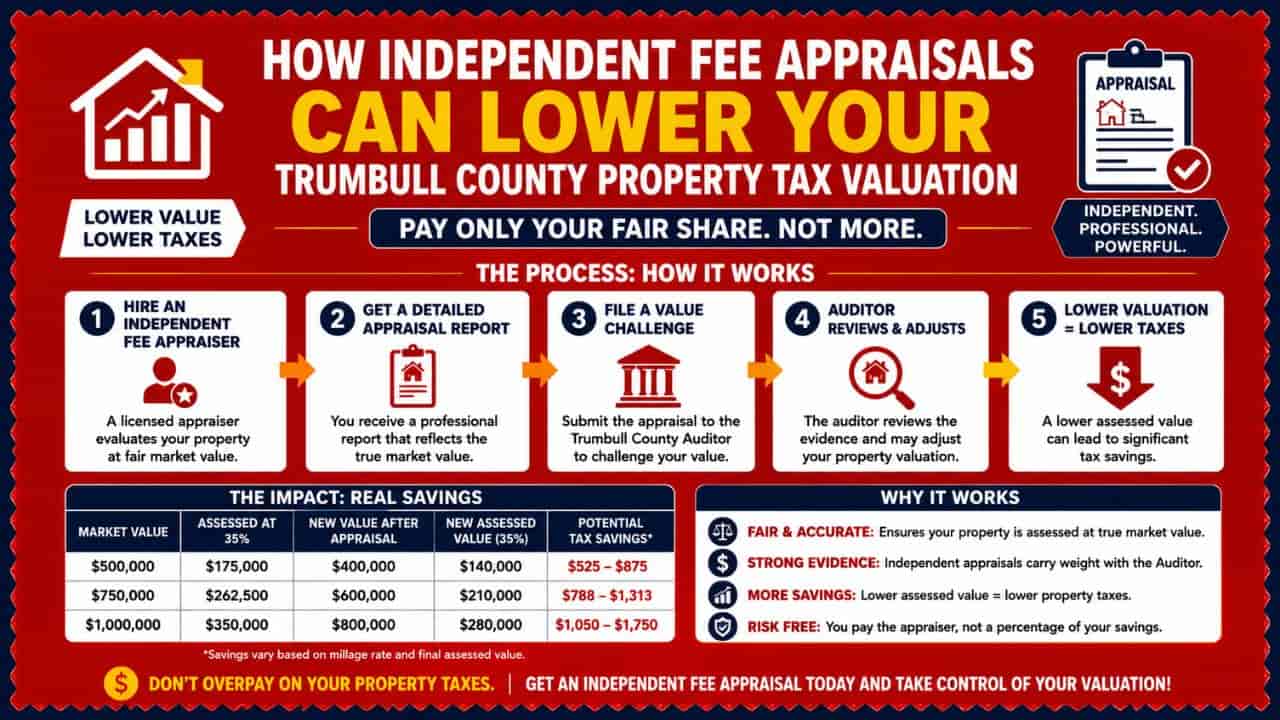

Step-by-Step Guide: Using an Appraisal to File a Property Tax Appeal

Navigating a formal tax dispute requires exact compliance with state timelines and documentation steps. Use this sequential breakdown to build a strong case.

Step 1. Review Your Official Property Record Card via the Online Portal: (Obtain Property Record).

Access the Trumbull County Auditor’s online portal and pull your property record card. Check the structural specifications for errors, such as incorrect square footage, inflated room counts, or inaccurate construction years.

Step 2. Commission an Independent, Certified USPAP Appraisal: (Hire an Ohio Certified Appraiser).

Hire a state-licensed appraiser. Explicitly inform them that the appraisal report is for a property tax appeal, ensuring the valuation date targets exactly January 1st of the disputed tax year.

Step 3. Complete and File DTE Form 1 with the Board of Revision: (File DTE Form 1).

Fill out DTE Form 1 (Complaint Against the Valuation of Real Property). State your requested value clearly, attach a full copy of the appraisal report as supporting evidence, and submit it before the statutory deadline.

Step 4. Attend the Scheduled Board of Revision Hearing: (Present Evidence).

Present your case to the BOR panel. Bring extra printed copies of your appraisal report. Focus your argument purely on objective market evidence and structural data, avoiding emotional appeals about tax rates.

| Appraisal Firm Name | Physical Office Address | Core Specialization & Contact |

| John Tricomi & Associates, Inc. | 608 Robbins Avenue, Niles, OH 44446 | Commercial, Industrial, and Multi-Family tax appeals. Phone: (330) 394-9999 |

| Morganstern Appraisal Service | 2831 Silver Fox Dr SW, Warren, OH 44481 | Certified Residential Valuations and Board of Revision filings. Phone: (330) 824-8377 |

| Ed Cline Appraisals | Serving Trumbull County Environs (Northeast Ohio) | Multi-Family Property Challenges and Regional Townships. Phone: 1-888-ED CLINE |

Strategic Legal Timelines for Ohio Property Tax Appeals

Property owners must coordinate their administrative actions around a rigid statutory calendar. Missing these windows completely revokes your right to file an appeal for the current cycle.

- The Filing Window: The Board of Revision accepts DTE Form 1 submissions annually between January 1st and March 31st. Late applications are not accepted under any circumstances.

- The Valuation Date Anchor: Regardless of when your physical appraisal occurs during the spring, the valuation must explicitly reflect the property’s condition and market marketability on January 1st of the preceding tax year.

- The One-Filing Rule: Under Ohio law, property owners can generally only file a valuation complaint once in any given three-year triennial update cycle, making it essential to present your strongest appraisal proof during the initial hearing.

Conclusion

Challenging an inflated property tax assessment requires moving past generic market complaints and leaning on objective, professional real estate metrics. By securing an independent fee appraisal, Trumbull County property owners can effectively counter inaccurate mass appraisal models with reliable, localized documentation. Staying organized, meeting strict Board of Revision deadlines, and documenting structural liabilities ensures your property investments remain fairly assessed and financially secure over the long term.

FAQs

What is the deadline to file a valuation appeal in Trumbull County?

You must submit DTE Form 1 to the Board of Revision between January 1st and March 31st. Submissions postmarked after March 31st are automatically rejected.

Can I use an online home value estimate for my tax appeal?

No. Local boards routinely reject automated online valuations. Ohio administrative rules require verified, market-adjusted evidence, making a certified USPAP appraisal report the standard for successful appeals.

Does an independent appraiser work for the county tax office?

No. Private fee appraisers are independent contractors licensed by the State of Ohio. They owe no allegiance to local county tax duplicate goals, ensuring an unbiased market valuation.

What happens if the Board of Revision denies my valuation appeal?

If you disagree with the local board’s decision, you can appeal the ruling within 30 days to the Ohio Board of Tax Appeals (BTA) or the local Court of Common Pleas.

Will a drop in property value lower my current year’s tax rate?

An appeal can lower your property’s assessed market valuation, which directly reduces your individual tax liability. However, it does not change the base voter-approved millage tax rates within your district.