Ohio’s real estate tax framework can appear deceptively complex when property owners receive their annual valuation statements. Inside Trumbull County, a common source of confusion stems from two distinct terms listed on tax sheets, gross millage and effective millage. These metrics dictate how your annual property tax liabilities are formulated across distinct local taxing jurisdictions. Because millage rates are heavily impacted by changing property values and community-voted school levies, understanding the structural layout of these indicators protects your home equity. This comprehensive guide outlines the operational differences between gross and effective rates, explains how state laws protect your wallet from inflation, and provides a step-by-step roadmap to auditing your local tax calculations.

What Is a Mill? Understanding the Basis of Ohio Property Tax

Before diving into the variations of gross and effective rates, it is critical to define the foundational unit of measurement: the mill. In real estate taxation, a “mill” represents one-tenth of a cent, which translates mathematically to $1 of tax for every $1,000 of a property’s assessed, taxable valuation.

The Assessed Value Rule

Under Ohio state law, you never pay property taxes on 100% of your home’s appraised fair market value. Instead, the county auditor locks your assessed taxable value at exactly 35% of the full appraised market value.

Taxable Value = Appraised Fair Market Value x 0.35

If your residential property in Warren, Ohio, is appraised by the auditor at $200,000, your local effective and gross tax calculations are strictly applied to an assessed base of $70,000.

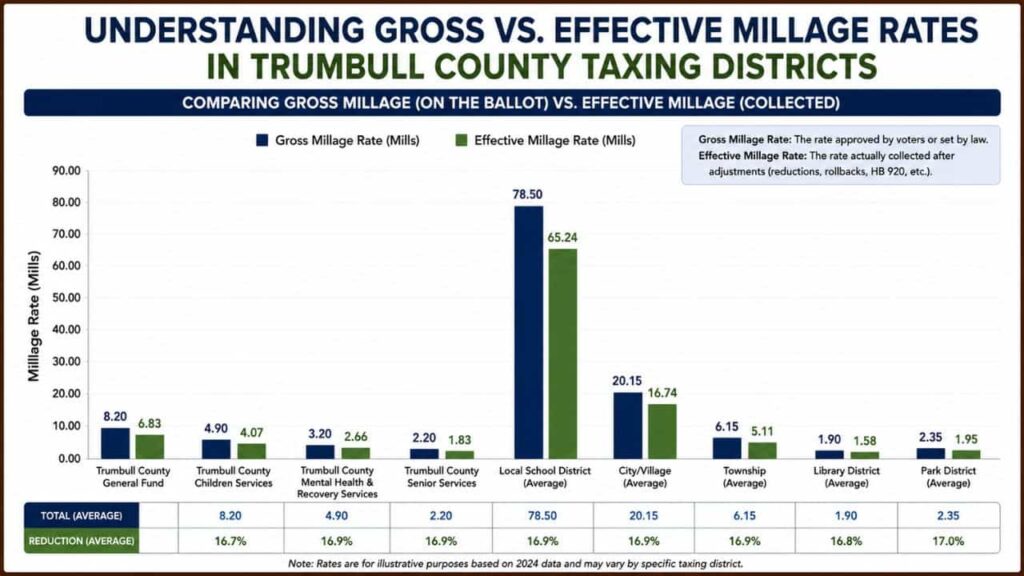

Gross Millage vs. Effective Millage: The Core Differences

Your total annual property tax bill is a combination of multiple separate levies passed by your county, township, city, and local school district. However, the rates are adjusted differently based on voter approval and legislative action.

Defining Gross Millage Rates

Gross millage is the absolute base rate of taxation established within a specific community. It represents the sum total of all “inside millage” (the baseline 10 mills allowed by the Ohio Constitution without voter approval) combined with the full, original millage amounts approved by local voters through past ballot levies. Think of gross millage as the starting point before any legal rollbacks are calculated. This rate is virtually never used to calculate your actual out-of-pocket tax bill.

Defining Effective Millage Rates

Effective millage is the actual rate applied directly to your property’s taxable value to determine the final amount you owe. It represents the gross millage rate after state-mandated tax reduction factors have been applied. As neighborhood property values scale upward due to real estate demand or sexennial reappraisals, these reduction factors decrease the effective millage rate to prevent local government agencies from collecting windfall revenues.

How House Bill 920 Regulates Millage Rate Adjustments

The structural buffer separating gross millage from effective millage exists because of a historic piece of legislation known as House Bill 920 (HB 920), enacted in 1976.

The Voter Levy Protection Mechanism

When voters in a Trumbull County school district pass a property tax levy designed to collect a fixed sum for example, $2 million annually for campus security HB 920 dictates that the levy can only collect that original $2 million target each year, regardless of market movements.

If local property assessments boom across the township, the county auditor must deploy a tax reduction factor to roll back the millage rate. This mathematical compression causes your effective millage to drop significantly below the original gross millage voted on at the ballot box.

Inside Millage: The Exception to the Rule

It is vital to note that HB 920 rollbacks do not apply to the constitutional 10 mills of inside millage. Because inside mills are continuous and non-voted, their effective rate matches their gross rate exactly. When real estate appraisals climb, the revenue generated from inside millage rises proportionally, which funds core county operational infrastructure.

System Infrastructure: Trumbull County vs. Stark County Portals

To evaluate how these tax components affect your individual parcel, county authorities provide public databases. Tracking how these rates are published requires interacting with independent county software systems.

For example, the Trumbull County Auditor’s real estate search platform allows users to pull up specific taxing district summaries to view the historical split between gross and effective millage rates across different townships.

When evaluating operational data delivery models across Ohio, comparing regional system structures provides vital clarity for property owners.

| Taxing Infrastructure Component | Gross Millage System Mandate | Effective Millage System Mandate | County Application & Data Architecture |

| Trumbull County Auditor Portal | Displays the full unvoted inside 10 mills plus original voter-approved rates. | Computes automated reduction factors following real estate value updates. | Offers interactive spatial and tabular lookups tailored to local school precincts. |

| Stark County Auditor Portal | Maintained as a baseline reference index for long-term levy approvals. | Serves as the actual multiplying factor against 35% assessed values. | Provides a structured guide for auditor services to track rolling levy performance. |

| Ohio Department of Taxation | Verifies legal maximum thresholds for multi-district municipal levies. | Signs off on finalized statutory reduction factor values annually. | Ensures uniform equalization across all 88 independent Ohio counties. |

Step-by-Step Guide: How to Calculate Your Property Tax Bill

If you want to audit your tax bill manually to verify that the auditor’s office is applying the correct effective millage parameters, follow this professional step-by-step mathematical calculation sequence.

Step 1. Extracting Your Total Appraised Market Value: Locate Value.

Log onto your local county property portal. Search your property by name or parcel ID to identify the full market valuation established during the latest appraisal cycle.

Step 2. Calculating Your 35% Assessed Taxable Value Base: Apply Assessment.

Multiply your total appraised fair market value by 0.35. For an asset appraised at $150,000, this calculation locks your taxable base at exactly $52,500.

Step 3. Isolating the Effective Millage for Your Specific District: Identify Rates.

Go to the taxing district rate sheet on the auditor’s platform. Identify your district’s active effective millage rate (do not use the gross millage figure).

Step 4. Applying the Millage Calculation to Formulate Base Tax: Execute Formula.

Divide your effective millage rate by 1,000, then multiply that decimal by your assessed taxable value base to arrive at your annual property tax total before credits.

Key Administrative Solutions for Resolving Tax Discrepancies

If your physical tax statement reflects an incorrect millage rate application, or if you believe a local school levy has been miscalculated against your parcel boundaries, consider these professional remedies:

- Request a Taxing District Verification:

Contact the auditor’s fiscal department to double-check that your home is assigned to the correct municipal precinct. Boundary lines can occasionally shift, placing properties in incorrect school tax brackets. - Audit Your Active Owner-Occupancy Credits:

Ensure you are receiving your 2.5% owner-occupied tax reduction if the home serves as your primary residence, as this credit applies directly to eligible local voter levies. - File an Official Board of Revision Dispute:

If the core problem is an inflated property appraisal driving up your inside millage liabilities, file DTE Form 1 with the Board of Revision before the statutory March 31 deadline to lower your taxable baseline.

Conclusion

Mastering the difference between gross millage and effective millage rates across Trumbull County taxing districts is a vital step for every property owner. Under Ohio state law, utilizing advanced systems like the Trumbull County Auditor and Stark County Auditor portals allows citizens to audit their assessed taxable value and understand how House Bill 920 tax reduction factors protect their real estate investments from inflationary spikes.

FAQs

What is gross millage in Trumbull County, Ohio?

Gross millage is the baseline tax rate approved by local voters or allowed by the state constitution before applying any statutory reduction factor rollbacks.

How does effective millage calculate my property tax bill?

Effective millage is the actual rate multiplied against your 35% assessed value, adjusted downward by tax reduction factors to keep government revenues flat when property values rise.

What does House Bill 920 do for property owners?

House Bill 920 prevents inflation from increasing voter-approved fixed-sum levies by scaling down effective millage rates as countywide real estate appraisals increase.

How do Trumbull and Stark County auditors differ in millage tracking?

Both operate as independent fiscal watchdogs under Ohio law, using specialized software and services guides to automatically compute spatial tax rates and parcel records.

Can my effective millage rate change without voter approval?

Yes. When local property appraisals change during an auditor’s sexennial reappraisal or triennial update, effective millage rates automatically recalculate to balance the books.